AI’s Next Bottleneck in Financial Services Is Infrastructure

Published on: 05/15/2026

By Sidhartha Menon

SHARE

Table Of Contents

- The Cloud-first Decade Solved The First Problem

- Why Financial AI Needs A Different Infrastructure Conversation

- The Rise Of Specialised GPU Deployment

- Different Financial Institutions Will Adopt Differently

- India Already Has A Proof Point

- The Economics Will Decide The Business Model

- What Makes This Vc-fundable

- The Next Phase Of Financial Intelligence

This week on Eximius Echo, we’re looking back at the signals, sectors, and nine new bets that shaped our year.

If you’re new here, Eximius is a pre-seed VC fund backing bold ideas in ConsumerTech, FinTech, and Enterprise AI.

Let’s dive in.

Financial services has always been a hard category for new technology to enter. The systems are older, the data is sensitive, and the cost of failure is brutal.

Yet today, banks, NBFCs, fintechs, and payment companies are paying close attention to AI. The use cases are no longer restricted to chatbots or surface-level automation. AI is entering customer support, fraud detection, credit scoring, KYC workflows, compliance checks, document processing, employee productivity, and portfolio intelligence.

The reason is simple. Financial services runs on decisions. AI can make those decisions faster, cheaper, and more contextual.

But a deeper question emerges: “Can the current infrastructure stack actually support production-grade financial AI?”

The Cloud-first Decade Solved The First Problem

For the last decade, hyperscalers such as AWS, Microsoft Azure, and Google Cloud have become the default infrastructure layer.

They made compute elastic, shifted infrastructure from capex to opex, and gave companies access to storage, security, APIs, identity, analytics, and deployment tools without forcing them to build data centres.

For fintechs, cloud allowed teams to scale during transaction spikes, launch products faster, and focus engineering bandwidth on customer experience instead of hardware maintenance.

But financial AI is starting to stretch the limits of generic cloud infrastructure.

Why Financial AI Needs A Different Infrastructure Conversation

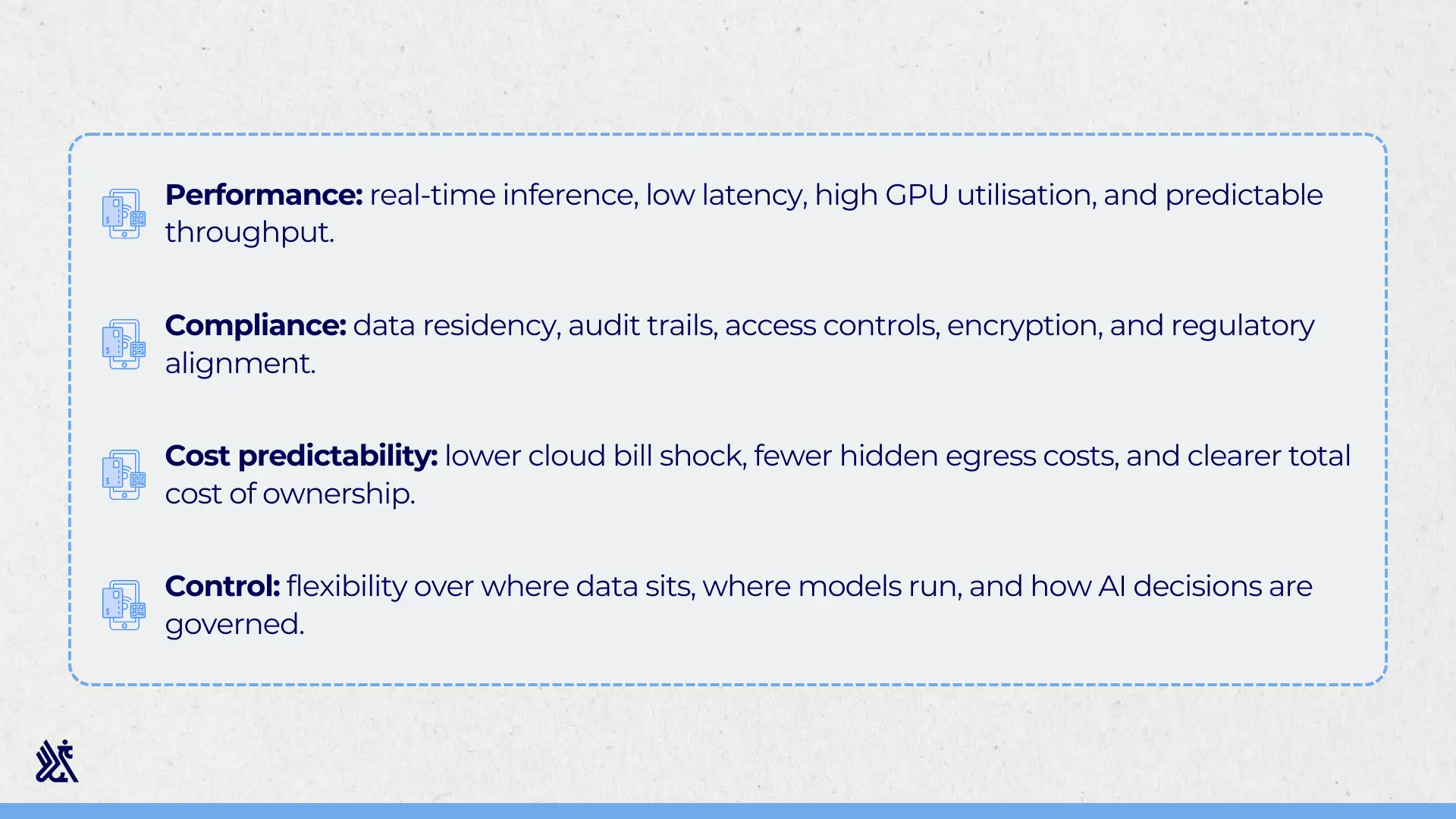

AI workloads in financial services are different from traditional SaaS workloads. A fraud system cannot afford latency spikes. A KYC workflow cannot expose sensitive customer data. A payments assistant cannot hallucinate through a transaction dispute.

The infra layer now has to deliver four things together:

This is where hyperscalers start to feel less natural for financial AI.

Shared cloud environments can make performance less predictable. Dollar-linked billing can make costs harder to forecast. And while storing data in India solves one part of the problem, banks still need control over access, governance, auditability, and model deployment. This gap is creating a new category of AI infrastructure.

The Rise Of Specialised GPU Deployment

India-first GPU cloud providers, sovereign cloud providers, and specialised AI infra companies are building environments designed for training, fine-tuning, inference, and regulated deployment.

The market already has early leaders. Neysa is building a sovereign AI execution layer for training, fine-tuning, and production deployment. E2E Networks is making INR-denominated GPU cloud more accessible for Indian AI teams. Yotta’s Shakti Cloud is targeting institutional-scale AI workloads. The whitespace, therefore, is not in basic GPU access alone. It sits in bundled, BFSI-ready infrastructure that combines compute, compliance, security, orchestration, and managed services.

Bare-metal GPU access reduces abstraction. NVLink, InfiniBand, and direct-attached storage improve performance. Rupee-denominated billing and local hosting make cost and compliance easier to manage.

The shift is from generic elasticity to workload-specific performance. That matters because AI in finance will not be one uniform workload.

Different Financial Institutions Will Adopt Differently

Large banks are likely to follow a hybrid, control-first path. Sensitive workloads like ledgers, credit scoring, fraud detection, and PII-heavy systems will stay on-premise or private, while front-facing channels, chatbots, and marketing analytics can continue on cloud.

Mid-tier banks and NBFCs may become the most aggressive adopters of specialised AI infrastructure. For them, GPU-as-a-service, AI cloud layers, vector databases, RAG systems, and document intelligence tools can unlock faster KYC, loan origination, and customer service workflows.

Small finance banks and cooperative banks may take a more SaaS-led or community-cloud route. The Indian Financial Services Cloud and sovereign AI providers can help them access secure, local AI infrastructure without carrying the full cost of building it internally.

This adoption curve will be segmented. Each customer type will need a different product, price point, and deployment model.

Most incubation centers follow a multi-step process that may include an initial online application, detailed business plan submissions, pitch presentations to a panel and in some cases, in-person interviews. Selection committees typically comprise industry veterans, government officials, domain specialists and sometimes successful entrepreneurs. Evaluation criteria focus on innovation, scalability, socio-economic impact and alignment with the incubator’s sectoral priorities.

Founders must also be prepared for location specific requirements. A startup incubation centre in Gujarat may prioritize manufacturing related or exportf ocused innovations, while one in Karnataka might lean toward deep tech or AI-driven solutions. Additionally, some state programs expect a tangible contribution to the local economy or community. Being aware of these nuances allows founders to tailor applications with precision, increasing their chances of acceptance and ensuring they enter an incubator environment aligned with their growth strategy.

India Already Has A Proof Point

NPCI’s FiMi shows where this market can go.

FiMi is a payments-native AI model built for Indian financial workflows. It supports transaction disputes, mandate lifecycle management, and multilingual interfaces across English, Hindi, Hinglish, Telugu, and Bengali. It powers the UPI Help Assistant and shows that financial AI in India needs domain-specific data, local context, high-volume reliability, and infrastructure that can operate inside regulated payment systems.

This is the larger signal: India’s financial AI stack will need models that understand Indian money movement, Indian languages, Indian compliance, and Indian scale.

The Economics Will Decide The Business Model

Cloud and APIs work well when AI usage is still experimental. But once workloads become predictable and always-on, the cost equation changes.

For the same sustained AI workload, owned infrastructure can be treated as the baseline cost. Running it on AWS can cost roughly 7x more, while API-based access can cost roughly 22x more.

The lesson is simple: when utilisation is high, infrastructure ownership or specialised deployment can become a major cost advantage.

This matters for financial AI because fraud detection, risk monitoring, KYC processing, customer support, and compliance automation can run continuously. These are the workloads where infrastructure design becomes a margin lever.

What Makes This Vc-fundable

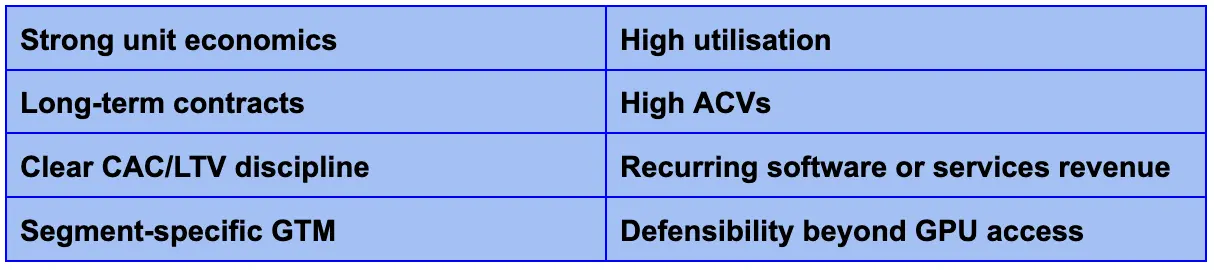

Pure GPU resale is a thin business. The opportunity becomes interesting when a company builds a bundled software and services layer around the hardware.

That could mean GPU orchestration, deployment tooling, monitoring, compliance workflows, inference optimisation, model governance, managed services, or vertical AI stacks for specific BFSI customers.

The strongest companies will show:

In this category, the underwriting question is simple: Can the company turn a capex-heavy infrastructure layer into a high-margin, sticky, recurring platform?

The Next Phase Of Financial Intelligence

The last phase of fintech was application-led. Dashboards, apps, chatbots, digital onboarding, and analytics defined the surface area. The next phase will be infrastructure-led.

As AI becomes embedded inside decisions, financial institutions will need to decide where intelligence lives, how it is governed, and what architecture allows it to scale safely. The winners in this market will combine performance, compliance, and capital efficiency.

In Indian BFSI, AI infrastructure will become a strategic layer. Compute, data, models, and governance will sit at the centre of how financial institutions build trust, reduce cost, and compete in real time.

If you’re building at the intersection of AI, infrastructure, financial services, or regulated workflows, write to us at [email protected]. We’d love to hear what you’re building.

Sidhartha Menon

Investment Associate